At first glance, adding more features to a model seems like an obvious way to improve performance. If a model can learn from more information, it should be able to make better predictions. However, in practice, this trend often introduces hidden structural risks. Each additional feature creates another dependency on upstream data pipelines, external systems, and data quality checks. A single missing field, schema change, or delayed dataset can silently degrade predictions in production.

The deeper issue is not computational cost or system complexity – it is weight instability. In regression models, especially when features are correlated or weakly informative, the optimizer struggles to make attributions in a meaningful way. As the model attempts to distribute effects over overlapping signals, coefficients may change unexpectedly, and low-signal variables may appear significant due to noise in the data. Over time, this leads to models that look sophisticated on paper but behave inconsistently when deployed.

This article examines why adding more features can make regression models less reliable rather than more accurate. The sections below explore how correlated features distort coefficient estimates, how weak signals get mistaken for real patterns, and why each additional feature increases the delicacy of the output. To solidify these ideas, the following examples use asset pricing datasets and compare the behavior of large “kitchen-sink” models with more static alternatives.

importing dependencies

pip install seaborn scikit-learn pandas numpy matplotlibimport numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import matplotlib.gridspec as gridspec

import seaborn as sns

from sklearn.linear_model import Ridge

from sklearn.preprocessing import StandardScaler

from sklearn.metrics import mean_squared_error

from sklearn.model_selection import train_test_split

import warnings

warnings.filterwarnings("ignore")

plt.rcParams.update({

"figure.facecolor": "#FAFAFA",

"axes.facecolor": "#FAFAFA",

"axes.spines.top": False,

"axes.spines.right":False,

"axes.grid": True,

"grid.color": "#E5E5E5",

"grid.linewidth": 0.8,

"font.family": "monospace",

})

SEED = 42

np.random.seed(SEED)

This code sets a clean, consistent Matplotlib style by adjusting background colors, grid appearance, and removing unnecessary axis spines for clear visualization. It also sets a fixed NumPy random seed (42) to ensure that any randomly generated data remains reproducible throughout the run.

synthetic asset dataset

N = 800 # training samples

# ── True signal features ────────────────────────────────────

sqft = np.random.normal(1800, 400, N) # strong signal

bedrooms = np.round(sqft / 550 + np.random.normal(0, 0.4, N)).clip(1, 6)

neighborhood = np.random.choice((0, 1, 2), N, p=(0.3, 0.5, 0.2)) # categorical

# ── Derived / correlated features (multicollinearity) ───────

total_rooms = bedrooms + np.random.normal(2, 0.3, N) # ≈ bedrooms

floor_area_m2 = sqft * 0.0929 + np.random.normal(0, 1, N) # ≈ sqft in m²

lot_sqft = sqft * 1.4 + np.random.normal(0, 50, N) # ≈ sqft scaled

# ── Weak / spurious features ────────────────────────────────

door_color_code = np.random.randint(0, 10, N).astype(float)

bus_stop_age_yrs = np.random.normal(15, 5, N)

nearest_mcdonalds_m = np.random.normal(800, 200, N)

# ── Pure noise features (simulate 90 random columns) ────────

noise_features = np.random.randn(N, 90)

noise_df = pd.DataFrame(

noise_features,

columns=(f"noise_{i:03d}" for i in range(90))

)

# ── Target: house price ─────────────────────────────────────

price = (

120 * sqft

+ 8_000 * bedrooms

+ 30_000 * neighborhood

- 15 * bus_stop_age_yrs # tiny real effect

+ np.random.normal(0, 15_000, N) # irreducible noise

)

# ── Assemble DataFrames ──────────────────────────────────────

signal_cols = ("sqft", "bedrooms", "neighborhood",

"total_rooms", "floor_area_m2", "lot_sqft",

"door_color_code", "bus_stop_age_yrs",

"nearest_mcdonalds_m")

df_base = pd.DataFrame({

"sqft": sqft,

"bedrooms": bedrooms,

"neighborhood": neighborhood,

"total_rooms": total_rooms,

"floor_area_m2": floor_area_m2,

"lot_sqft": lot_sqft,

"door_color_code": door_color_code,

"bus_stop_age_yrs": bus_stop_age_yrs,

"nearest_mcdonalds_m": nearest_mcdonalds_m,

"price": price,

})

df_full = pd.concat((df_base.drop("price", axis=1), noise_df,

df_base(("price"))), axis=1)

LEAN_FEATURES = ("sqft", "bedrooms", "neighborhood")

NOISY_FEATURES = (c for c in df_full.columns if c != "price")

print(f"Lean model features : {len(LEAN_FEATURES)}")

print(f"Noisy model features: {len(NOISY_FEATURES)}")

print(f"Dataset shape : {df_full.shape}")This code produces a synthetic dataset designed to mimic a real-world asset pricing scenario, where only a few variables actually affect the target while many others introduce redundancy or noise. The dataset contains 800 training samples. Key signal characteristics such as square footage (square feet), number of bedrooms, and neighborhood category represent the primary drivers of home prices. In addition to these, many derived features are deliberately created to be highly correlated with the key variables – e.g. floor_area_m2 (a unit conversion of square footage), lot_squarefootand total_rooms. These variables simulate multicollinearity, which is a common problem in real datasets where multiple features carry overlapping information.

The dataset also contains weak or spurious features – e.g. door_color_code, bus_stop_age_yearsAnd nearest_mcdonalds_m-which have little or no meaningful relationship with the price of the property. To further replicate the “kitchen-sink model” problem, the script generates 90 completely random noise features, representing irrelevant columns that often appear in large datasets. The target variable value is constructed using a known formula where square footage, bedrooms, and neighborhood have the strongest influence, while bus stop age has little influence and random noise introduces natural variability.

Finally, two feature sets are defined: a lean model containing only the three real signal features (squarefoot, bedroom, neighborhood) and a noisy model containing every available column except the target. This setup allows us to directly compare how a minimal, high-signal feature set performs against a larger, feature-heavy model filled with redundant and irrelevant variables.

How Multicollinearity Destabilizes Coefficients

print("n── Correlation between correlated feature pairs ──")

corr_pairs = (

("sqft", "floor_area_m2"),

("sqft", "lot_sqft"),

("bedrooms", "total_rooms"),

)

for a, b in corr_pairs:

r = np.corrcoef(df_full(a), df_full(b))(0, 1)

print(f" {a:20s} ↔ {b:20s} r = {r:.3f}")

fig, axes = plt.subplots(1, 3, figsize=(14, 4))

fig.suptitle("Weight Dilution: Correlated Feature Pairs",

fontsize=13, fontweight="bold", y=1.02)

for ax, (a, b) in zip(axes, corr_pairs):

ax.scatter(df_full(a), df_full(b),

alpha=0.25, s=12, color="#3B6FD4")

r = np.corrcoef(df_full(a), df_full(b))(0, 1)

ax.set_title(f"r = {r:.3f}", fontsize=11)

ax.set_xlabel(a); ax.set_ylabel(b)

plt.tight_layout()

plt.savefig("01_multicollinearity.png", dpi=150, bbox_inches="tight")

plt.show()

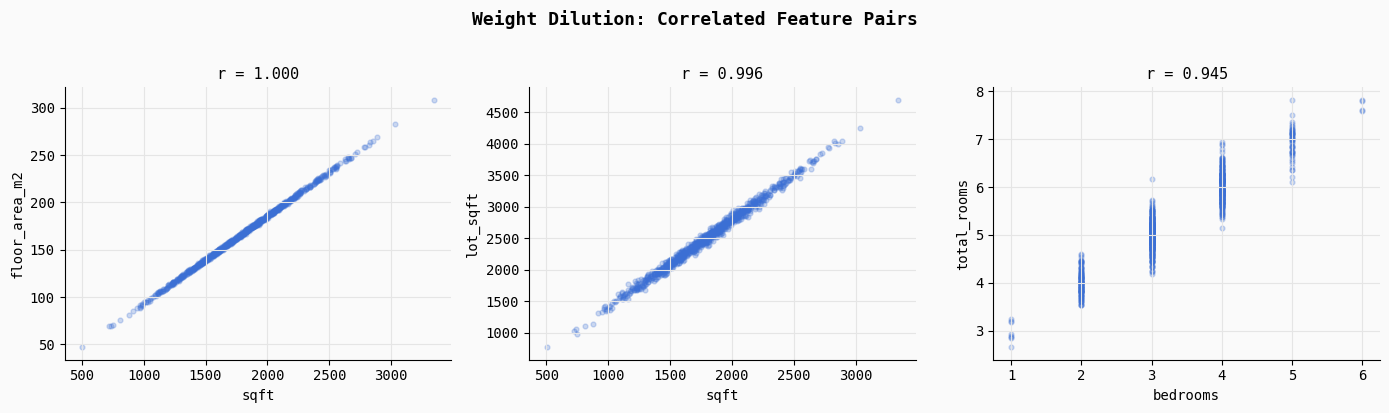

print("Saved → 01_multicollinearity.png")This section demonstrates multicollinearity, a situation where multiple features contain approximately the same information. The code calculates the correlation coefficient for three intentionally correlated feature pairs: sqft vs floor_area_m2, sqft vs lot_sqft, and bedrooms vs total_rooms.

As the printed results show, these relationships are extremely strong (R ≈ 1.0, 0.996, and 0.945), meaning that the model captures multiple signals describing the same underlying property characteristic.

Scatter plots visualize this overlap. Because these features move almost perfectly together, the regression optimizer struggles to determine which feature should get credit for predicting the target. Instead of assigning explicit weights to a variable, models often arbitrarily partition the effects across correlated features, leading to unstable and diluted coefficients. This is one of the major reasons why adding unnecessary features can make the model less interpretable and less stable, even if the predictive performance initially appears similar.

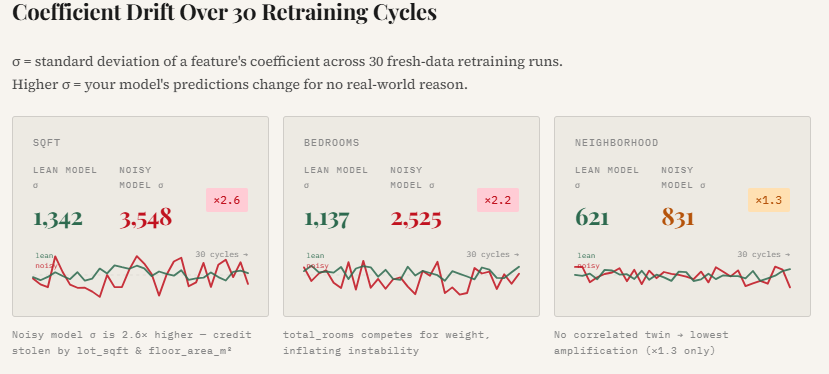

Weight instability in retraining cycles

N_CYCLES = 30

SAMPLE_SZ = 300 # size of each retraining slice

scaler_lean = StandardScaler()

scaler_noisy = StandardScaler()

# Fit scalers on full data so units are comparable

X_lean_all = scaler_lean.fit_transform(df_full(LEAN_FEATURES))

X_noisy_all = scaler_noisy.fit_transform(df_full(NOISY_FEATURES))

y_all = df_full("price").values

lean_weights = () # shape: (N_CYCLES, 3)

noisy_weights = () # shape: (N_CYCLES, 3) -- first 3 cols only for comparison

for cycle in range(N_CYCLES):

idx = np.random.choice(N, SAMPLE_SZ, replace=False)

X_l = X_lean_all(idx); y_c = y_all(idx)

X_n = X_noisy_all(idx)

m_lean = Ridge(alpha=1.0).fit(X_l, y_c)

m_noisy = Ridge(alpha=1.0).fit(X_n, y_c)

lean_weights.append(m_lean.coef_)

noisy_weights.append(m_noisy.coef_(:3)) # sqft, bedrooms, neighborhood

lean_weights = np.array(lean_weights)

noisy_weights = np.array(noisy_weights)

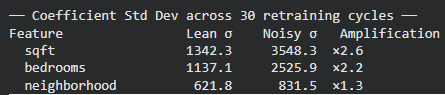

print("n── Coefficient Std Dev across 30 retraining cycles ──")

print(f"{'Feature':<18} {'Lean σ':>10} {'Noisy σ':>10} {'Amplification':>14}")

for i, feat in enumerate(LEAN_FEATURES):

sl = lean_weights(:, i).std()

sn = noisy_weights(:, i).std()

print(f" {feat:<16} {sl:>10.1f} {sn:>10.1f} ×{sn/sl:.1f}")

fig, axes = plt.subplots(1, 3, figsize=(15, 4))

fig.suptitle("Weight Instability: Lean vs. Noisy Model (30 Retraining Cycles)",

fontsize=13, fontweight="bold", y=1.02)

colors = {"lean": "#2DAA6E", "noisy": "#E05C3A"}

for i, feat in enumerate(LEAN_FEATURES):

ax = axes(i)

ax.plot(lean_weights(:, i), color=colors("lean"),

linewidth=2, label="Lean (3 features)", alpha=0.9)

ax.plot(noisy_weights(:, i), color=colors("noisy"),

linewidth=2, label="Noisy (100+ features)", alpha=0.9, linestyle="--")

ax.set_title(f'Coefficient: "{feat}"', fontsize=11)

ax.set_xlabel("Retraining Cycle")

ax.set_ylabel("Standardised Weight")

if i == 0:

ax.legend(fontsize=9)

plt.tight_layout()

plt.savefig("02_weight_instability.png", dpi=150, bbox_inches="tight")

plt.show()

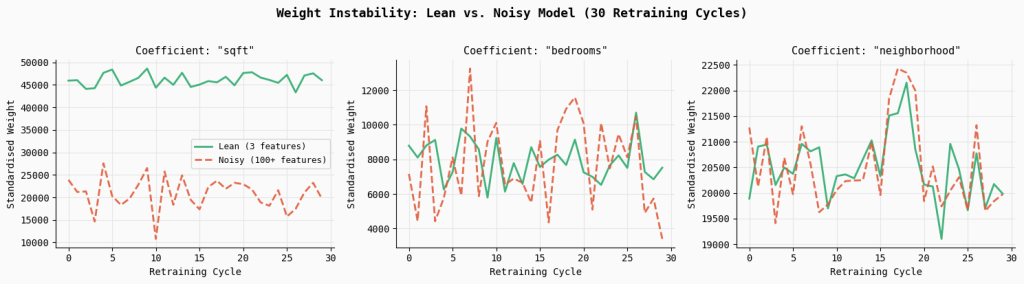

print("Saved → 02_weight_instability.png")This experiment simulates what happens in real production systems where models are periodically retrained on fresh data. Over 30 retraining cycles, the code randomly samples a subset of the dataset and fits two models: a lean model using only the three core signal features, and a noisy model using the full feature set containing correlated and random variables. By tracking the coefficients of key features in each retraining cycle, one can see how stable the learned weights remain over time.

The results show a clear pattern: the noisy model exhibits quite high coefficient variability.

For example, the standard deviation of the square footage coefficient increases by 2.6×, while bedrooms become 2.2× more volatile than in the Lean model. The plotted lines make this effect clearly evident – the coefficients of the lean model remain relatively smooth and consistent across re-training cycles, while the weights of the noisy model fluctuate much more. This instability arises because correlated and irrelevant features force the optimizer to redistribute credit unpredictably, making the model’s behavior less reliable, even if the overall accuracy appears to be the same.

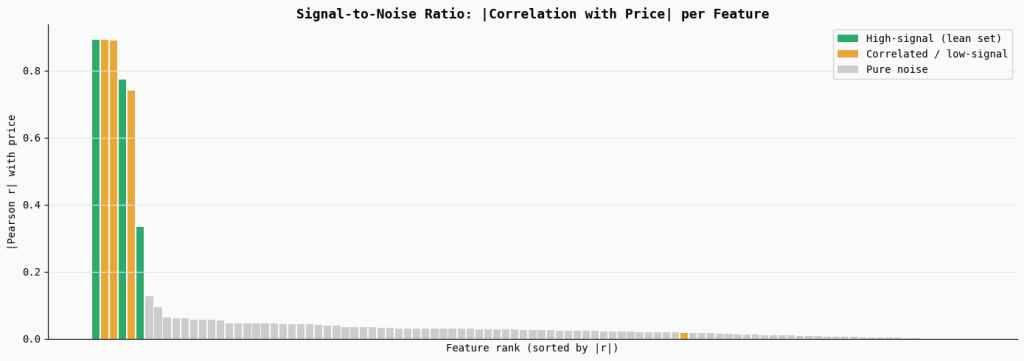

Signal-to-noise ratio (SNR) degradation

correlations = df_full(NOISY_FEATURES + ("price")).corr()("price").drop("price")

correlations = correlations.abs().sort_values(ascending=False)

fig, ax = plt.subplots(figsize=(14, 5))

bar_colors = (

"#2DAA6E" if f in LEAN_FEATURES

else "#E8A838" if f in ("total_rooms", "floor_area_m2", "lot_sqft",

"bus_stop_age_yrs")

else "#CCCCCC"

for f in correlations.index

)

ax.bar(range(len(correlations)), correlations.values,

color=bar_colors, width=0.85, edgecolor="none")

# Legend patches

from matplotlib.patches import Patch

legend_elements = (

Patch(facecolor="#2DAA6E", label="High-signal (lean set)"),

Patch(facecolor="#E8A838", label="Correlated / low-signal"),

Patch(facecolor="#CCCCCC", label="Pure noise"),

)

ax.legend(handles=legend_elements, fontsize=10, loc="upper right")

ax.set_title("Signal-to-Noise Ratio: |Correlation with Price| per Feature",

fontsize=13, fontweight="bold")

ax.set_xlabel("Feature rank (sorted by |r|)")

ax.set_ylabel("|Pearson r| with price")

ax.set_xticks(())

plt.tight_layout()

plt.savefig("03_snr_degradation.png", dpi=150, bbox_inches="tight")

plt.show()

print("Saved → 03_snr_degradation.png")This section measures the signal strength of each feature by calculating its absolute correlation with the target variable (price). The bar chart ranks all features based on their correlation, highlighting the true high-signal features in green, correlated or weak features in orange, and the larger set of pure noise features in gray.

Visualization shows that only a few variables provide meaningful predictive signals, while most contribute none. When too many low-signal or noisy features are included in a model, they dilute the overall signal-to-noise ratio, making it harder for the optimizer to consistently identify the features that really matter.

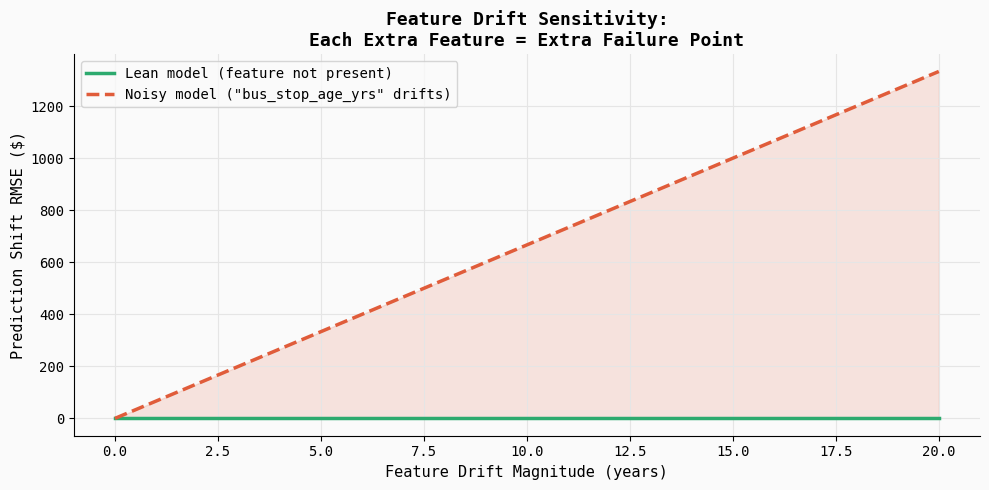

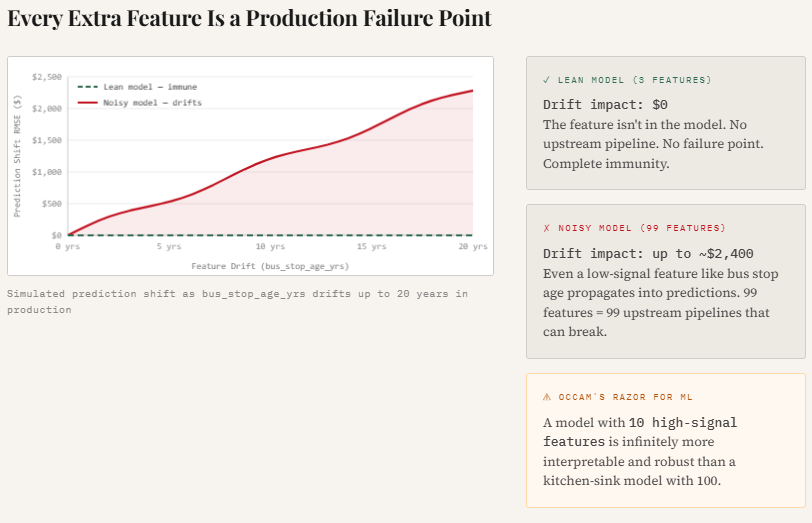

Feature Drift Simulation

def predict_with_drift(model, scaler, X_base, drift_col_idx,

drift_magnitude, feature_cols):

"""Inject drift into one feature column and measure prediction shift."""

X_drifted = X_base.copy()

X_drifted(:, drift_col_idx) += drift_magnitude

return model.predict(scaler.transform(X_drifted))

# Re-fit both models on the full dataset

sc_lean = StandardScaler().fit(df_full(LEAN_FEATURES))

sc_noisy = StandardScaler().fit(df_full(NOISY_FEATURES))

m_lean_full = Ridge(alpha=1.0).fit(

sc_lean.transform(df_full(LEAN_FEATURES)), y_all)

m_noisy_full = Ridge(alpha=1.0).fit(

sc_noisy.transform(df_full(NOISY_FEATURES)), y_all)

X_lean_raw = df_full(LEAN_FEATURES).values

X_noisy_raw = df_full(NOISY_FEATURES).values

base_lean = m_lean_full.predict(sc_lean.transform(X_lean_raw))

base_noisy = m_noisy_full.predict(sc_noisy.transform(X_noisy_raw))

# Drift the "bus_stop_age_yrs" feature (low-signal, yet in noisy model)

drift_col_noisy = NOISY_FEATURES.index("bus_stop_age_yrs")

drift_range = np.linspace(0, 20, 40) # up to 20-year drift in bus stop age

rmse_lean_drift, rmse_noisy_drift = (), ()

for d in drift_range:

preds_noisy = predict_with_drift(

m_noisy_full, sc_noisy, X_noisy_raw,

drift_col_noisy, d, NOISY_FEATURES)

# Lean model doesn't even have this feature → unaffected

rmse_lean_drift.append(

np.sqrt(mean_squared_error(base_lean, base_lean))) # 0 by design

rmse_noisy_drift.append(

np.sqrt(mean_squared_error(base_noisy, preds_noisy)))

fig, ax = plt.subplots(figsize=(10, 5))

ax.plot(drift_range, rmse_lean_drift, color="#2DAA6E",

linewidth=2.5, label="Lean model (feature not present)")

ax.plot(drift_range, rmse_noisy_drift, color="#E05C3A",

linewidth=2.5, linestyle="--",

label="Noisy model ("bus_stop_age_yrs" drifts)")

ax.fill_between(drift_range, rmse_noisy_drift,

alpha=0.15, color="#E05C3A")

ax.set_xlabel("Feature Drift Magnitude (years)", fontsize=11)

ax.set_ylabel("Prediction Shift RMSE ($)", fontsize=11)

ax.set_title("Feature Drift Sensitivity:nEach Extra Feature = Extra Failure Point",

fontsize=13, fontweight="bold")

ax.legend(fontsize=10)

plt.tight_layout()

plt.savefig("05_drift_sensitivity.png", dpi=150, bbox_inches="tight")

plt.show()

print("Saved → 05_drift_sensitivity.png")This experiment demonstrates how feature drift can silently influence model predictions in production. The code introduces gradual drift into a weak feature (bus_stop_age_yrs) and measures how much the model’s predictions change. Since the lean model does not include this feature, its predictions remain completely stable, whereas the noise model becomes increasingly sensitive as drift magnitude increases.

The resulting plot shows that the prediction error continues to increase as the feature changes, highlighting an important production reality: each additional feature becomes another potential failure point. Even low signal variables can introduce instability if their data distribution changes or upstream pipelines change.

Limitations and what to watch

The experiments here use a synthetic dataset, which makes the effects of redundant and low-signal features easy to see but does not capture every complication of real data, such as nonlinear relationships, interaction effects, or non-stationary distributions. Coefficient instability is most pronounced in linear and regularization-sensitive models; tree-based and ensemble methods respond to redundant features differently and may mask the problem rather than expose it. The broader takeaway is practical rather than absolute: more features are not automatically better, and feature selection, regularization, and monitoring of coefficient stability over retraining cycles are worthwhile safeguards. Results on any specific production system should be validated against that system’s own data before acting on them.